Most credit unions are leaving money on the table — not because they lack good members, but because their underwriting can't keep up.

Manual decisioning is slow, inconsistent, and expensive. The average loan officer spends 3–4 hours per application on data gathering alone. That's a cost center masquerading as a process.

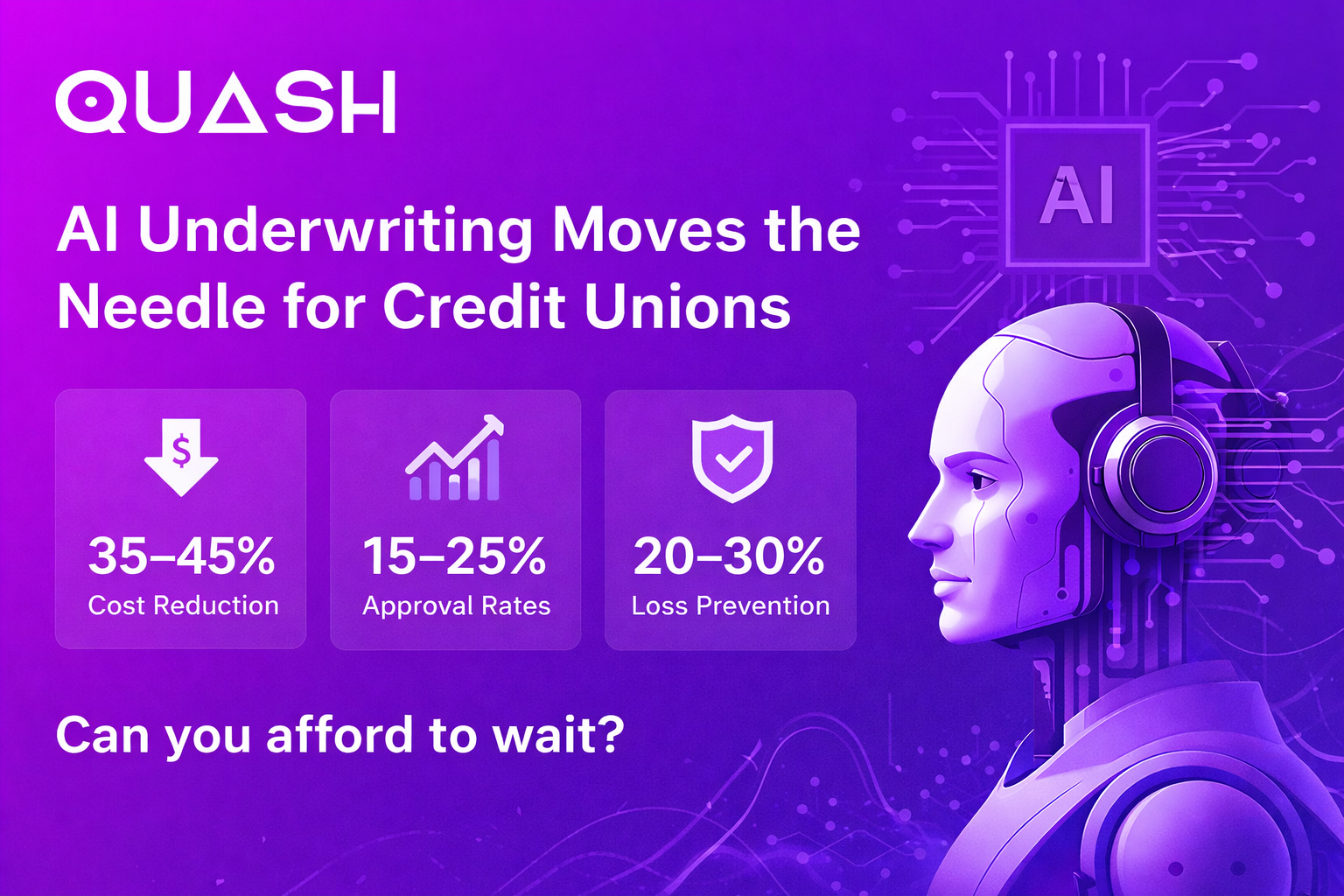

Where AI underwriting moves the needle:

Cost reduction:

Automating the data pull, risk scoring, and initial decisioning cuts per-loan processing costs by 35–45%. At 10,000 loans/year, that's a meaningful line item.

Approval rates:

Traditional credit scores miss the full picture. AI models trained on alternative data — cash flow patterns, payment history, employment stability — approve 15–25% more creditworthy applicants that rule-based systems reject.

Loss prevention:

Better risk segmentation means lower charge-offs. Credit unions using predictive models see default rates drop 20–30% in the first year — without tightening standards.The business case isn't complicated.

Faster decisions mean members don't go to the bank down the street. Fewer defaults mean a healthier balance sheet. More approvals mean more revenue from the members you already have.

The question isn't whether AI underwriting has ROI. It's whether your credit union can afford to wait.

.svg)